[ad_1]

Does Microfinance Actually Improve Lives?

December 5, 2022

Microfinance, once hailed as a miracle solution, has become the subject of skepticism in the last several years. There is no doubt that repayment rates are as high or higher than traditional financing, but many questioned whether these loans actually led to improvements in individual and family living conditions.

For the first time, Wisconsin Microfinance has been able to track what truly matters, and is measuring changes in the quality of life of borrowers over the first 18 months after receiving a loan.

Preliminary survey results were gathered from a small set of our borrowers (36 borrowers) in Haiti. Participants were surveyed with a series of questions three times: 1) prior to taking the first loan, 2) prior to taking out a second loan (after paying the first back), and 3) prior to taking out a third loan (after paying the second back).

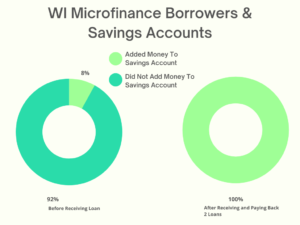

We begin with the inspiring result in Figure 1 that the percentage of borrowers who reported they had added money to a savings account in the last year increased from 8% (prior to receiving a loan financed by WI Microfinance loan) to 100% (after receiving – and paying back – two loans financed by WI Microfinance), showing that all of our borrowers were not only better able to meet daily needs, but also prepare for their futures.

Figure 1

Figure 1

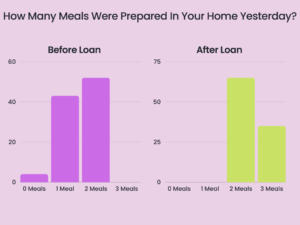

We then turn to the impact of receiving a loan on food security. Before receiving their loans, 4% of borrowers did not prepare a meal in their house the day prior to the survey, with an additional 42% reporting that only one meal was prepared. In Survey 2, after receiving a first round loan, no one responded that 0 or 1 meals were prepared in their homes the day prior, and 100% of borrowers had access to 2 or 3 meals the previous day. These improved results continued into the third survey, showing dramatically positive impacts. As for clean water, one of the most fundamental of human needs, we found that prior to receiving their first loan, 8% of borrowers sourced their drinking water from a river, making them susceptible to water borne disease and contamination. After the first loan, none of the borrowers obtained water from the river, and instead used a mixture of community and personal wells.

Figure 2

Figure 2

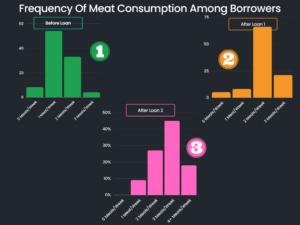

Prior to taking the first loan, as seen in Figure 3, 54% (the majority) of loan recipients reported eating only one meal a week containing meat (beef, pork, chicken, or fish). After one loan, 87% of respondents indicated that they ate meat two or three times a week. After a second loan, these numbers had again improved with an additional 17% saying they were eating meat 4 or more times a week. Overall, the consumption of meat, chicken, and fish (typically heartier, more expensive foods) increased significantly.

Figure 3

Figure 3

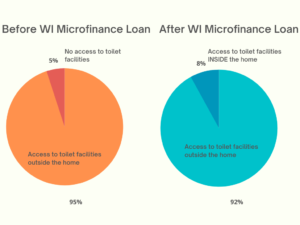

We next moved to one of the most basic of needs – toilet facilities. Figure 4 shows that in the initial survey, 95% of borrowers reported that they had access to toilet facilities, but that these were outside the home. One respondent reported not having toilet facilities at all. After the first loan, 92% of borrowers reported having toilet facilities outside the home, while the remaining 8% had access to toilet facilities inside the home. No one reported not having toilet facilities. These results stayed consistent even during the third survey, eight months later.

Figure 4

Figure 4

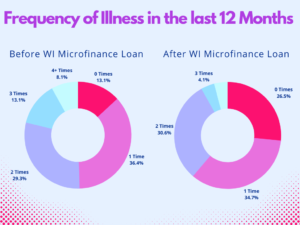

Figure 5 showcases improved health and wellness as a measure of quality of life. When tracking the frequency of illness, we found that prior to receiving their first loan, 13% stated that within the last 12 months no one had gotten sick. The remaining responses were distributed over reports of someone getting sick one, two, three or more times. By the second survey, almost 27% of respondents stated that no one had gotten sick over the previous 12 months, indicating a significant improvement in health that is correlated with greater access to funds.

Figure 5

Figure 5

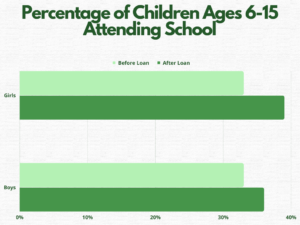

We then moved towards education. As we see in Figure 6, the percentage of boys ages 6-15 attending school at least once a week increased from 33% to 36%. For girls, this percentage increased from 33% to 39%.

Figure 6

Figure 6

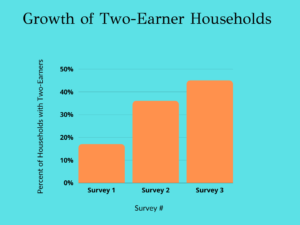

Wisconsin Microfinance targets loans to women, so we expect to see an increase in the number of “breadwinners”, or people that bring money to a household. As we see in Figure 7, initially 83% of borrowers reported that only 1 person brought in money (for most households, this would have been the male). At the second survey, the percentage of single breadwinner households decreased to 63%. By the third survey, only 55% reported a single breadwinner for the family.

Figure 7

Figure 7

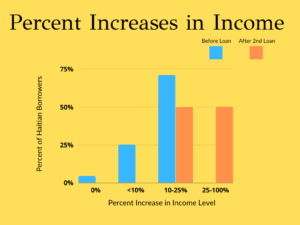

When it comes to the easier to measure aspects, like changes in income, we found positive results as well. Before the first loan, 70% of loan recipients reported that their income had increased 10 – 25% during the previous 12 months. No one reported their income increasing more than 25%. After the first loan, 40% of loan recipients reported their income increasing 25 – 100%. These numbers held up after paying back their second loan, where again, 40% of loan recipients reported that their income had increased 25 – 100% over the past 12 months.

Figure 8

Figure 8

It is important to note that the results also contain unexplainable data. In the initial survey, 83% of borrowers reported owning the homes, but in the second survey, this number had dropped to 78% before bouncing back up to 100% in the third survey. Data irregularities may be a function of who was filling out the survey, or other unanticipated changes in quality of life that were uncorrelated with the loans. However, Wisconsin Microfinance believes that our loans truly are representing a hand-up, not a hand out. The overwhelming majority of results show a measurable increase in quality of life for Wisconsin Microfinance borrowers, suggesting that microfinance may be even more effective than once thought, and can truly have a remarkable impact on people’s lives.

Author: Jahnvi Datta

[ad_2]